Share

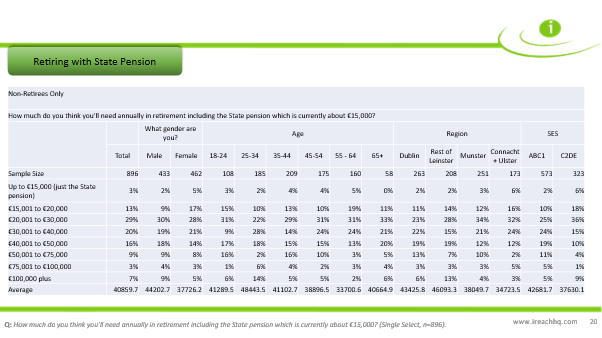

Adults in Ireland who have yet to retire think they’ll need €40,860 on average a year – the equivalent of about three-quarters the average Irish wage[1] – to get by in retirement. However, men believe they’ll need significantly more than women, expecting to require an annual retirement income of €44,000 on average, compared to €38,000 for women.

The new nationwide survey of 900 non-retirees of all ages, by Royal London Ireland[2], one of Ireland’s leading life insurance and pensions companies, shows that the vast majority (97%) of people who have yet to retire in Ireland believe that the State pension alone is not enough to get by on in retirement.

Commenting on the survey findings, Mark Reilly, Pension Proposition Lead at Royal London Ireland said,

“People often underestimate the amount of savings required for a comfortable retirement – as well as the expenses they will face during this phase of life. Our research found that, on average, people believe they will need €40,860 a year in retirement.

"Given that a report published in [3] found that a single person would need a pension of €33,600 a year, and that a couple would need €43,200 a year for a comfortable retirement, even allowing for inflation since then, the €40,860 income doesn’t seem that far off the mark. However, whether or not people can secure whatever annual pension they are expecting will really depend on how they approach pension saving.

“While the overwhelming majority (97%) of people who are yet to retire don’t expect to be able to get by in retirement on €15,000 a year, which is close to the current State pension, a recent report from the CSO found that around one third of workers don’t have a private pension and mostly expect to rely on the State pension[4]. Auto-enrolment should certainly help boost pension coverage but for many workers, the pension delivered by auto-enrolment may not deliver a sufficient income in retirement.”

On- or off-target with pension savings?

Taking the average amount of income which the survey found people expect in retirement (€40,860), experts at Royal London Ireland calculated[5] how much saving would be required to hit that target, assuming that the individual qualifies for the full State pension (Contributory), which is currently €15,564 a year[6].

- To achieve a retirement income of €40,860 by the current State pension age of 66, an individual on a salary of €61,908 who starts their pension at the age of 30 would need to save the equivalent of 22% of their salary a year – the equivalent of €1,135 a month[7].

- If the individual was 35 when they started saving into their pension, they would need to save the equivalent of 27% of their salary a year - the equivalent of €1,393 a month[8].

- If that individual started their pension at the age of 40, they would need to save the equivalent of 34% of their salary a year – the equivalent of €1,754 a month[9].

Commenting, Mr Reilly said:

“People’s aspirations of the income they will need in retirement often doesn’t match up to what their pension savings will deliver. Previous research by Royal London Ireland found that three-quarters of people underestimate the amount they would need to fund a modest pension in retirement[10]. People’s lack of awareness of how much it would take to secure a modest pension means many are unlikely to put enough aside in pensions contributions through their working life.”

Great expectations

According to the Royal London Ireland survey, one in ten (10%) expect to need between €75,000 and €100,000 a year or more. The research also found that expectations of the amount of money needed in retirement vary widely, depending on age, gender, marital status and where an individual is living:

- Men are almost twice as likely as women to say they would need an income of €100,000 plus when they retire (9% versus 5%).

- While numbers are small, more than twice as many women than men expect to be able to get by on the equivalent of the State pension in retirement (5% versus 2%), with the working class[11] three times as likely as the middle class[12] to say the same (6% versus 2%).

- Those aged between 25 and 34 believe they will need the most income in retirement, with this age cohort expecting to need an annual income of €48,443 on average when they retire (see Table 1).

- At €41,289 on average, those aged 18-24 had the second highest expectations of the amount of income they would need in retirement.

- The amount of income which people think they will need in retirement decreases with age. Those aged between 55 and 64 believe they will need the least amount of money when they retire, with this age cohort believing that €33,701 on average would be enough annual income in retirement. This compares to an average of €38,896 for 45-54 year-olds and €41,103 for 35-44 year-olds.

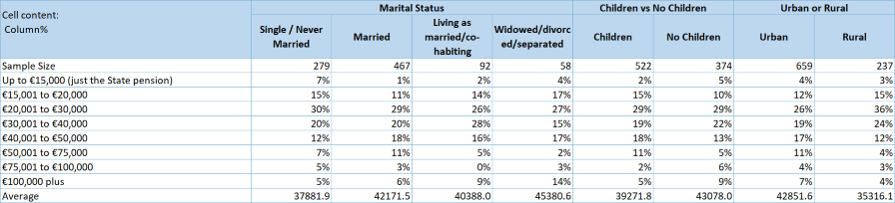

- Single people ‘lowball’ what they’ll need in retirement compared to their peers who are in relationships, with the average singleton expecting to need €37,882 in retirement compared to an average of €42,171 for married individuals (see Table 3 in Appendix).

- Divorced, separated or widowed individuals expect to need more income in retirement than their married counterparts, with €45,381 being the average income which this group expect to need at retirement, compared to €42,171 for married individuals.

- Those who don’t have children expect to need more income in retirement than those who do. On average, €39,272 was the amount that those with children believe would be sufficient income to get by on in retirement, and this compared to €43,078, for those without children.

- Residents of Leinster (excluding Dublin) expect to need on average €11,370 more by way of annual retirement income than those living in Connacht and Ulster. At an average of €46,093, those living in Leinster (excluding Dublin) have the highest expectation in terms of amount they feel they will need at retirement, while those living in Connacht and Ulster have the lowest, at €34,723 (see Table 1 in Appendix).

- When looking specifically at urban and rural dwellers, those living in urban areas expect to need €7,536 more on average a year in retirement income than their rural counterparts (€42,852 for urban dwellers versus €35,316 for rural dwellers).

Mr Reilly concluded,

“It’s clear from our survey that some people ‘highball’ the amount of income they’re likely to need in retirement and that others ‘lowball’ it. There can be many things shaping people’s expectations around the income they will need in retirement – such as their standard of living and income during their working life, their age, their marital status, and even the cost of living in a rural area versus an urban area. Regardless of what is influencing one’s expectations of the amount of money they’ll need in retirement, it’s important that these expectations are reasonable and realistic. It’s crucial that people have a realistic understanding of their financial needs and the time available to build sufficient savings to cover what they’ll need in retirement. Otherwise, they could be in for a significant financial shock when they retire and could even struggle to make ends meet.

“Independent financial advice from a Financial Broker is invaluable here as it will help people calculate how much money they will need in retirement and how much they will need to save to reach that target.”

- ENDS -

[1] According to the CSO’s latest Earnings & Labour Costs figures, published at the end of Feb 2026, which put the average wage at €52,618 a year or €1,011.88 a week in Quarter 4 2025.

[2] Conducted by iReach on 1,000 adults, 896 of which were non-retirees

[3] Irish Pension Council Report on Irish Retirement Living Standards, published September 2024

[4] As per CSO Pension Coverage Report 2025, published in April 2026

[5] Using the Pensions Authority calculator, which uses certain assumptions to calculate savings required to hit a target pension.

[6] As the individual qualifies for the maximum State Pension of €15,564, the calculations outline how much would need to be saved by the individual to make up the €25,296 shortfall between €40,860 and €15,564, not the full amount of €40,860.

[7] Age-related limits on pension tax relief apply – see https://www.revenue.ie/en/jobs-and-pensions/pension/relief/tax-relief-limits.aspx - and this will limit how much of the €1,135 will qualify for tax relief.

[8] Age-related limits on pension tax relief apply – see https://www.revenue.ie/en/jobs-and-pensions/pension/relief/tax-relief-limits.aspx - and this will limit how much of the €1,393 will qualify for tax relief.

[9] Age-related limits on pension tax relief apply – see https://www.revenue.ie/en/jobs-and-pensions/pension/relief/tax-relief-limits.aspx - and this will limit how much of the €1,754 will qualify for tax relief.

[10] As per Royal London Ireland Press Release November 2020

[11] Class C2DE

[12] Class ABC1

Table 1

Table 2

Table 3

About Royal London Ireland

Royal London Ireland has a history of protecting its policyholders and their families, and it is committed to continue to do so for a long time to come. Our heritage in Ireland is 190 years starting when the Caledonian Insurance Company's first office opened on York Street, Dublin 2 in 1834. Today, Royal London Ireland is owned by The Royal London Mutual Insurance Society Limited – the UK’s largest mutual life insurance, pensions and investment company, and in the top 30 mutuals globally*, with assets under management of €228 billion, 8.5 million policies in force, and over 5,000 employees. Figures quoted are as at 31 December 2025.

Royal London Ireland’s office is based at 47-49 St Stephen’s Green, Dublin 2.

*Based on total 2022 premium income. ICMIF Global 500, 2024